The United States closed the first quarter of 2026 under the weight of two convergent data points that together signal a meaningful shift in the country’s economic trajectory. On 27 March, the University of Michigan released its final consumer sentiment reading for March, and on 25 March, Goldman Sachs revised its U.S. recession probability upward for the second time in less than a month. Taken together, the two releases confirm what individual indicators had been signalling for weeks: the American economy is entering a materially more fragile phase.

Sentiment Collapses Beyond Expectations

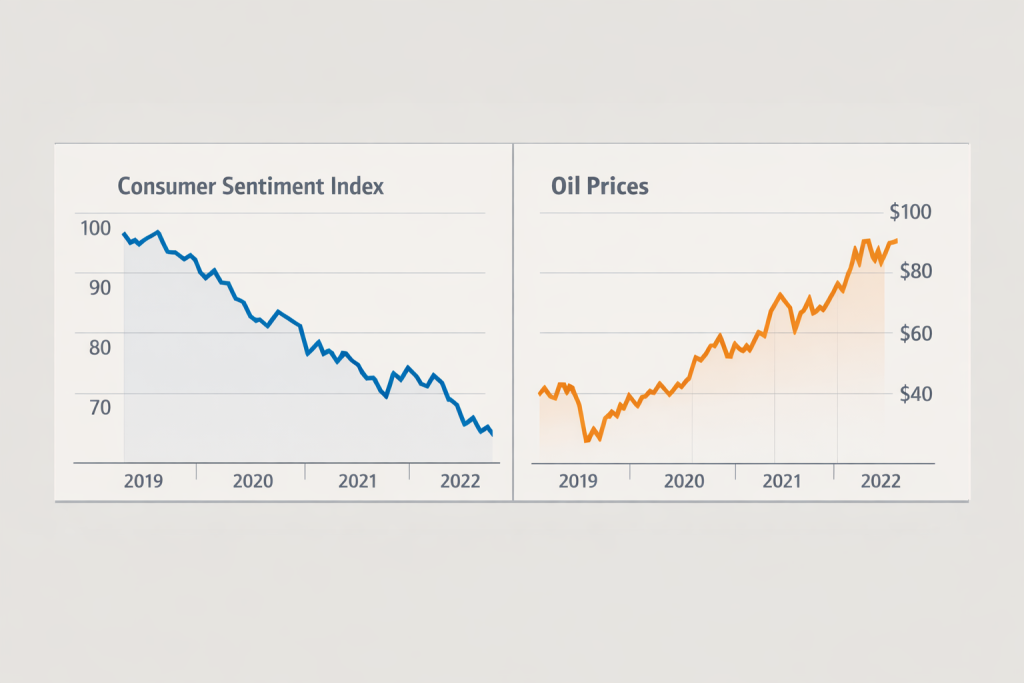

The University of Michigan Consumer Sentiment Index fell 6% in March to its lowest level since December 2025, with declines recorded across age groups and political affiliations. The final reading came in at 53.3 — missing the forecast of 55.5 and snapping a four-month streak of gains.

The breakdown is instructive. The short-term economic outlook fell 14%, and year-ahead expectations for personal finances declined 10%, while long-run expectations showed only modest deterioration — suggesting consumers do not yet expect current pressures to persist indefinitely. But that distinction offers limited comfort. Year-ahead inflation expectations rose to 3.8%, the largest monthly increase since April 2025.

Consumers with middle and higher incomes and stock wealth — buffeted by escalating gas prices and volatile financial markets following the Iran conflict — showed particularly large drops in confidence. This is significant because this cohort has historically been the segment most insulated from sentiment shocks; their deterioration points to conditions spreading beyond lower-income households.

Goldman Sachs Repositions the Recession Dial

The sentiment data did not arrive in isolation. On 25 March, Goldman Sachs raised its recession probability by 5 percentage points to 30%, while revising its headline PCE inflation forecast upward to 3.1% by December 2026 and nudging its full-year GDP growth estimate down to 2.1%.

Goldman’s shift reflects a confluence of pressures: the oil shock from Middle East tensions, with Brent crude climbing toward $100 and above; a labour market showing signs of fatigue; and fading fiscal support as the stimulative effects of prior policy actions roll off.

The bank’s economists have been explicit about the sequencing. The Federal Reserve held its policy rate steady at 3.5% to 3.75% at last week’s FOMC meeting — a decision Goldman characterised as somewhat more hawkish than expected — with Chair Jerome Powell placing employment and price concerns on equal footing and signalling that rate cuts remain possible but are not imminent.

That posture leaves the Fed in a position it is poorly equipped to navigate. Higher energy costs push inflation upward while simultaneously depressing growth — a combination that reduces the room for conventional monetary policy responses in either direction.

The Oil Shock as Primary Transmission Channel

The thread connecting sentiment, growth forecasts, and monetary uncertainty runs through energy markets. Events in the Middle East have materially altered the near-term economic and financial outlook, with S&P Global raising its 2026 inflation forecasts and lowering its growth projections across the board.

The conflict has choked off oil supply through the Persian Gulf — one of the most consequential energy supply disruptions in recent history — sending Brent crude from approximately $70 per barrel before the conflict to a peak near $119, before retreating to around $90. For U.S. consumers, that translated directly to gasoline prices approaching $4 per gallon nationally.

Economists note that if benchmark oil prices average around $125 per barrel over multiple months, recession risk rises sharply. While sustained levels at that threshold have not yet materialised, the warning underscores how closely energy markets and economic cycles are now linked.

Wall Street Is Not Unified

While Goldman’s 30% figure is significant for its institutional weight, the broader picture on Wall Street reflects a range of views. Recession odds on prediction markets have climbed to 39.2%, up from 22% at the start of March, while Moody’s forecasting model places the probability closer to 49%.

On the other side, BNP Paribas argues that the United States is well-positioned to absorb the shock, pointing to its status as the world’s largest crude producer and net energy exporter — a structural advantage that was absent during the oil shocks of the 1970s and 1980s.

Goldman itself continues to anticipate rate cuts in September and December, maintaining that a recession is not its base case — even as it acknowledges that growth could slow to between 1.25% and 1.75% annualised in the second half of 2026, a pace close to what economists describe as stall speed.

What the Quarter-End Signals

The United States enters the second quarter of 2026 carrying a specific set of pressures that were absent twelve months ago: an active energy supply disruption, a labour market that shed 92,000 jobs in February, a gold market that has delivered a year-to-date return of approximately 22%, and an S&P 500 down more than 3% for the quarter.

The April 6 diplomatic deadline between the U.S. and Iran represents the most immediate inflection point markets are tracking. A negotiated de-escalation would relieve pressure on energy prices and potentially allow the Fed to return to a rate-cutting posture. A prolonged conflict would cement the stagflationary dynamic and force a harder reassessment of corporate earnings forecasts, consumer spending trajectories, and debt sustainability for lower-income households carrying variable-rate obligations.

For now, the data is speaking clearly. Consumer confidence is at its weakest point in three months. The country’s most influential investment bank has raised its recession probability twice within thirty days. And the Federal Reserve is holding — unable to cut without inflaming inflation, and unwilling to raise without deepening the demand shock. Q2 will test whether that posture holds.